| Tue. May 26, 2026 |

|

|||

|

||||

| ||||

By Dr. David Phillips

Donald Trump has promised the American people that he will usher in a new dawn for America’s economy. As he announced during his address to a joint session of Congress on March 4, 2025, "We will have an economy that will be booming, maybe like we've never seen before."? This contrasted with what he said about Biden during his campaign: “over the past four years, Kamala and crooked Joe Biden have presided over an economic reign of terror, committing one financial atrocity after another.” There is of course no data to show that Trump’s promises of a boom are panning out, but to get a sense of the likely reality we can look at how Biden economic policies rated in comparison to Trump in his first term.

The Truth About The Economy And Jobs

There are many ways to measure the strength of an economy but output, employment and monetary stability (i.e. inflation) are critical, and they are the ones we look at here.

There was overall robust growth in GDP, production, and particularly jobs under Biden and a sustained boom in the stock market over 2022 to 2024. But there seemed, inexplicably, to be very little effective pushback by the Biden Administration against the Opposition’s relentless narrative that the economy was in a terrible mess. In fact, real GDP growth was positive after the COVID period and similar to that under Trump despite the lingering after-effects of the pandemic shock. In particular a widely predicted recession in 2023 was avoided probably due to astute Fed monetary policy. Growth continued without any let-up to the end of the Biden Presidency and into 2025.

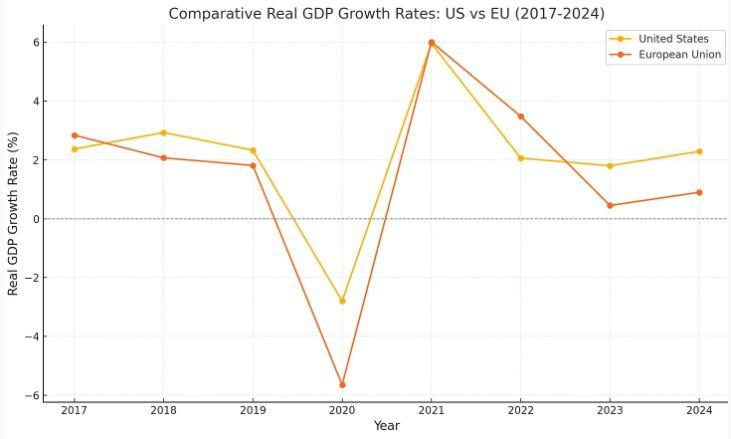

The following figure (from IMF and EU sources helps to understand growth under Trump and Biden but also compares it with what happened in comparable advanced economies (ones with competitive markets) in the European Union. The US and the EU growth pattern was overall similar over 2017 to 2024. For the US under Trump the real GDP rate of growth was level or falling slightly. After a very high growth rate recovery from the COVID pandemic in 2021 under Biden it settled at a level similar to the Trump years but well above that of the EU economies. This implied that, considering that it had to recover from a deep recession, the US economy under Biden was performing well not only compared to its past performance but also in maintaining international competitiveness.

Alongside GDP growth the record rise of the stock market, continuing into 2025, would have been hailed from the rooftops as a victory by a Republican party in power but was set aside by Democrats - fearing that celebration of capital gains would alienate wage-earners whom they still thought of as their voter base.

In the case of employment US performance under Biden was strong. Total employment rose by 17 million from the low point of the pandemic. At the start of the pandemic in early 2020 the rate of unemployment surged from a low 3.5% to over 10%. In January 2021 at the end of the first Trump presidency it had fallen back to about 6.5%, still historically high, but by January 2023 under Biden it fell to 3.4%, slightly below the rate prevailing pre-COVID. Since then for two years over 2023 to 2024 it averaged below 4%, the lowest sustained unemployment rate in the US since the 1970s. In the last, 48th, month of Biden’s Presidency job growth remained well above expectations at plus 256,000, while labor force participation rate was stable or rising.

Using data from the US Bureau of Labor Statistics (BLS) there was an increase in employment during the Trump period over 2017 to 2019, prior to the pandemic, averaging 1.5% per annum. This was significantly lower than the rate under Biden over 2021-24 which averaged just under 3% per annum. The 8.9 million jobs lost in the pandemic were fully compensated by the start of 2023. Out of the 17 million total jobs created about 7 million came after the end of the pandemic, that is, a 4.3% increase in total population employed over about 20 months.

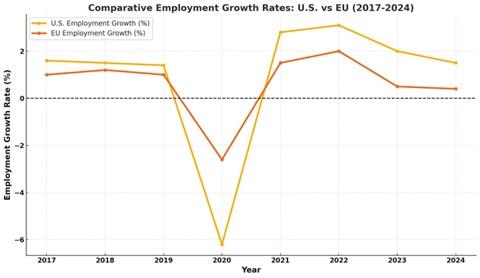

The chart below is based on IMF and EU official sources. The EU economies are again used as a comparator. The chart shows the US pandemic employment growth shock as being relatively severe (-6%) compared to the EU (-4.5%), but from 2021 the US rate of growth surged into positive territory above that of the EU. Not only was the average growth rate from 2021 significantly higher than the EU but it was also higher than the previous pre-pandemic rate achieved under Trump over 2017 to 2019, reflecting again the rapid US recovery from the pandemic under Biden.

The job growth shown rebuts the relentless Republican drumbeat that the growth was simply a pandemic rebound. This was false. Employment had recovered to the pre-COVID level and then continued to add jobs every month without a break. Trump also claimed in his 2024 convention speech that 100% of the new jobs post-pandemic were taken by illegal aliens. In fact, according to Forbes.com over 60% of the jobs are estimated to have gone to the US-born and more than another 20% to Green Card and work visa holders.

The Opposition also promised regularly that they would restore US manufacturing jobs. However, based on data from the BLS an estimated 172,000 manufacturing jobs were actually lost under Trump while 775,000 were added since January 2021 under Biden, partly because of the effects on investment of the Inflation Reduction Act and the Infrastructure Investment and Jobs Act (see below). The COVID employment shock was inevitably responsible for much of the decline under Trump, (so ‘not his fault’), but even after allowing for that the performance under Biden was better. In addition, real wages started to rise in 2023, helping to offset the problems for consumers caused by inflation.

The Biden Government passed major economic support legislation despite blocking efforts by the Opposition. The American Rescue Plan Act of 2021 was a very large economic stimulus of $1.9 trillion (about 8% of GDP) to help recovery from the pandemic, providing cash assistance, extending unemployment benefits, and expanding the Child Tax Credit, inter alia. The Infrastructure Investment and Jobs Act of 2021 funded $1.2 trillion for roads, bridges, public transit, and water systems; the CHIPS and Science Act of 2022 funded $280 billion of which over $50 billion was for semiconductor development; and, the Inflation Reduction Act of 2022 funded about $780 billion over 10 years for a package of climate change mitigation, healthcare, tax reform, and clean energy, plus action on drug prices and corporate taxes.

The American Rescue Plan was the most controversial of these programs as it most directly increased consumer demand and expenditure, while others such as the Infrastructure Act would have a longer-term impact. Democrat supporters believed that the Rescue Plan was necessary in order to help recovery from an unprecedented economic crisis affecting in particular poorer communities. Republicans, who voted against it on a party-line basis, claimed, largely on auto-pilot, that it was too late, inflationary, not well targeted, and that the extended unemployment benefits would encourage workers to avoid work. That is, a ‘welfare giveaway’.

The other programs included, at last, the major rebuilding of America’s dilapidated infrastructure, with the large number of jobs needed to do it, which Trump had promised but not delivered, and the planned revival of critical strategic production such as silicon chips and the wider development of advanced technology and AI, which Trump had also not got off the ground. Small Government subsidies reportedly were able to leverage private firms’ investment of tens of billions of dollars. There was $200 billion for federal STEM research and tax credits for U.S. semiconductor manufacturing, attracting large investors such as Taiwan’s giant semi-conductor manufacturer, TSCM. Production of advanced chips, batteries and solar panels have increased such that the US economy has risen strongly in the ranks of World manufacturers.

In the case of energy Trump stated at a campaign rally that he would “declare a national emergency to allow us to dramatically increase energy production, generation, and supply, which Comrade Kamala has destroyed.” In reality, American oil and gas production under Biden rose to record levels and the US has now, remarkably, become the World’s largest oil producer, larger even than Russia and Saudi Arabia, while at the same time renewable energy also increased significantly under Biden’s watch.

The relentless narratives about a Democrat economic disaster however had their effect, to the extent that the charges of incompetence were so ingrained in the beliefs of many that it was too late, come the election, to right the ship.

The Truth About Inflation.

The causes of the recent US inflation have stirred up a noisy discussion. A less serious part of the discussion was the charge by the Trump campaign that it “was the worst inflation in American history”. In fact the worst in recent memory occurred in the 1970s and early 1980s when it reached 12 to 15%.

The macro picture of the economy does not concern most people, but rising prices definitely do. Many voters blamed the Democrats not only for the high prices but also their supposed failure to bring them back down again.

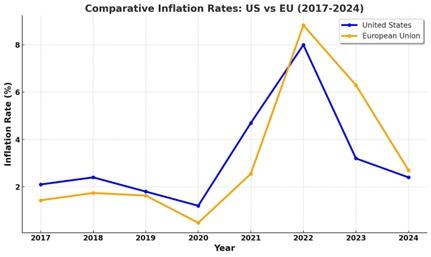

Different sources seem to show different, but comparable, results. The chart below is based on the BLS and Eurostat. It shows that over the three years 2017 to 2019 under Trump there was a low US inflation rate averaging just under 2% per annum. As the COVID pandemic started in early 2020 the inflation rate surged, reaching an annual 8% and a peak of 9.1% in June 2022. It then dropped steadily into the 2.5% range in 2024, with an uptick to 2.9% at the end of the Biden era, still close to the Fed target. For comparison, the US inflation rate had a similar pattern to the rate for the EU economies in its timing and trajectory over 4 years. It also had an almost identical inflation total over the four years, 20.8% against 20.4%. However, US inflation fell faster than the EU rate. This suggests that the US economy was behaving similarly to other market economies but recovering more quickly, probably because of more effective monetary control by the Fed.

For the US population at large however the average rate of inflation was not the problem, but rather how it affected specific products. The major price increases in services were in e.g. vehicle repairs and insurance, and in consumer goods it was foods such as margarine, juices and drinks, fats and oils, peanut butter, bread, sugar and eggs. All these rose 40% or more over the period 2020 to 2024, compared to the overall 20.4%. The largest item in the CPI index, about a quarter of the whole list, was rental costs which rose about 24.0%. The BLS also reported prices that fell, especially clothing and chinaware, and electronic goods such as computers and smartphones. The price of phones adjusted for quality fell by over 50% from 2020 to 2024.

In the US the high price of consumer goods suggested that the Government was not in control. Consumers paid attention to the individual, not the average price rises. But Europe had similar inflation spreads. Food prices there also rose rapidly, e.g. olive oil, sugar, biscuits, and butter saw major price hikes, some of over 70%, affected to a greater extent than the US by energy prices. The price rises between the US and the EU were similar in scale, trajectory and pattern of individual prices, and so they could not reasonably be pinned on the policies of a particular Government, as was the usual Republican refrain.

Nevertheless, in the US a polarized debate has emerged. Republican elements blamed the inflation on the effect of excessive economic stimulus spending through the ‘socialist’ COVID relief programs, especially the American Rescue Plan. The Democrat side in turn claimed that the major cause was, as in Europe, the supply disruptions of the pandemic and also a shift from services to goods like home equipment resulting from the lockdowns. According to Politifact, while there is agreement among economists that the relief cash may have resulted an increase of about 2% over the COVID-led inflation rate, the bulk of the increase was the result of the supply shocks, aggravated by rising energy prices.

A recent study (led by Peter Orzag of Lazards) has in fact been quite convincing in showing that the inflationary surge was more likely the result mainly of the disruption of supply. This conclusion is because of the obvious fact that inflation was a world-wide effect of the pandemic, and that several more advanced economies such as the UK and Germany experienced the same or worse price inflation than the US despite not having large relief packages in relation to their GDP. The US inflation was equal to or lower than that of nearly half of all countries despite the large relief spending. The fact that US inflation also fell more quickly from its peak of June 2022 compared to several other advanced economies is also not consistent with what might be expected from large scale public expenditure..

These factors suggest that the Government’s relief program was not the main cause of the inflation and the America Recovery Plan could not be described simply as a reckless Democrat giveaway. Whatever the case however the cause of inflation was never properly explained to the public apart from some initial, half-hearted, arguments by the Administration that it was transitory, which got heavily rebutted. But in the end the Government it seems may have been right about it being transitory, dying down after COVID treatments and vaccines arrived. US inflation fell rapidly from its peak of in June 2022, faster than many other advanced economies. At the same time real wage increases since 2023 helped to relieve the pressure on families, along with the historic increase in jobs. The Economist, a center-right-wing magazine, described the revival of the US economy during Biden’s watch as ‘the envy of the world.’

The failure of the Government’s economic argument was due greatly to a lack of organization. The President and his top advisers on the economy seemed rarely to go out in front of the cameras to explain the issues, leaving the door open to a relentless, cynical, opposition narrative of incompetence. One response proposed by Harris’s campaign, to introduce a law to prevent ‘price gouging,’ was probably seen by voters as a fig-leaf. The New Yorker, commenting on the lack of popular understanding of the Government’s economic program, wrote just before the election, of a: “vast gulf between its scale ... and its political impact, which is essentially zero …”

Inflation was managed successfully by the Administration but this was never announced. The President’s most effective addresses on the economy seem to have been delivered several weeks after the election was lost. A firm and convincing rebuttal could probably have stemmed the tide of criticism and the damage to the Democrats’ electoral chances.

First appeared in EVIDENCE, REASON AND GASLIGHT -

Subscribe at davidphillips502.substack.com

| Comments in Chronological order (0 total comments) | |

| Report Abuse |

| Contact Us | About Us | Donate | Terms & Conditions |

|

All Rights Reserved. Copyright 2002 - 2026